Bob Moritz, Chairman of the PwC Network, shares a preview of PwC’s 23rd Annual Global CEO Survey with a focus on rising chief executive pessimism and uncertainty heading into 2020.

Key highlights:

More than half (53%) of CEOs believe the rate of global economic growth will decline;

The share of CEOs very confident in their 12-month growth prospects fell to 27%, the lowest level since 2009;

Uncertainty around regulation, trade, and economic growth contribute to the decline in CEO confidence;

CEOs are divided over whether government legislation will splinter the internet;

18% of organizations globally cite significant progress in establishing an upskilling program.

20 to 30 years ago, a TMS was able to transact FX, interest rate transactions, single manual treasury payments, its reporting with MT940 for a financial status and liquidity planning, netting, guarantees. Usually, today there are also mass payments with all the user rights, audit trails, and many other things.

Will Vendor Finance themes a module of a TMS? Or also fraud detection?

Is it important to include supply chain features in a TMS as a module? I guess yes.

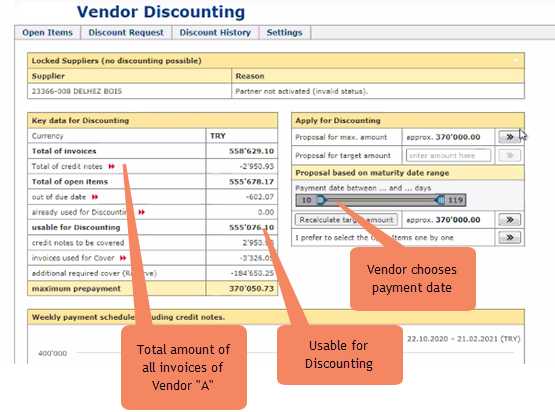

Recently, I joined a session of a local Swiss Vendor Financing Tool, which is implemented and runs at a bigger corporation as internal browser software. Each local entity of that corporate has the feature to deal with its local supplier and local banks into that Vendor-Finance-System. Once pre-negotiated with suppliers and banks, basic data are set up by the Group Treasury, then local suppliers and local banks can use their data within their contract area and in a way that allows the supplier to choose his own payment date.

Would it make sense to include such a system in a TMS? Can this be the future?

Listen to the podcast at TreasuryManagement.com where Coupa and Bellin discuss the TMS-future – Donna Wilczek, Coupa Software, François Masquelier, Simply Treasury, and Martin Bellin, BELLIN.

The podcast is 33 minutes long; due to the length to listen, it is unfortunate that the podcast has no minute-agenda-indication to flip to a preferred theme.

In den EU-Mitgliedsstaaten bilden die PSD2 Richtlinien seit September 2019 die Grundlage für Nicht-Banken mit Schnittstellen am Zahlungsverkehr teilzunehmen. Als nicht-PSD2 Mitglied besteht für die schweizerischen Finanzinstitute keine Verpflichtung zur Bereitstellung von Schnittstellen. Finanzinstitute und Drittanbieter können die Bedingungen für das offene Bankgeschäft selbst gestalten und sich aktiv an der Entwicklung neuer Geschäftsmodelle einbringen.

In der Schweiz laufen verschiedene Initiativen, um die Option Open-Banking zu schaffen. Siehe Tomato‘s Fachbericht

Die Schweizerische Bankiervereinigung erachtet den gegenwärtigen marktorientierte Ansatz als vorteilhaft. Es gibt noch zahlreiche Herausforderungen, wie Professor Dr. Andreas Dietrich von der Hochschule Luzern in einem Blog beschreibt.

Gegenwärtige Lösungen von Software-Anbietern:

Avaloq.one mit über 100 Fintechs an Bord

Offene Plattform Finnova

Open-Banking-Plattform Lenzburg/Finstar

Swisscom Open Banking Hub

b.Link der SIX unterstützt von Klara, Credit Suisse, Neue Aargauer Bank, UBS und ZKB

8. Abbildung von Cash Flow Hedges in der OR-Rechnungslegung

In vorherigen Tomato Catchup News haben wir Ihnen mehrere Berichte von KPMG’s Dr. Silvan Loser übermittelt. Verschiedene Leser haben diese Berichte besonders geschätzt. In einem neuen Artikel befasst sich Dr. Loser mit Hedge Accounting.

Der Autor erklärt den QR-Abrechnungsprozess in einem 32-seitigen Bericht. Hauptthemen: